How Much Money Does A Disabled Person Get

©GOBankingRates

Are you a risk-taker when it comes to your finances? Or, do you save money with your long-term future in mind?

No matter your saving style, one thing is for sure: Americans, in general, are not saving enough. In fact, GOBankingRates' latest savings survey found nearly 70 percent of Americans have less than $1,000 in a savings account. If your savings account is near empty, the problem could be your saving style.

"Those who save simply because they believe that they should save, tend to do so no matter what," said Kyle J. McCauley, managing partner at City Center Financial. "They put 5 percent or 10 percent of their paycheck in a separate account, every time, and just let the money sit there. They have no particular goal, other than to consistently save money. These individuals often amass savings accounts in the tens to hundreds of thousands of dollars."

We ranked six prominent types of savers, from least to most effective. Discover your own personal saving style, and learn how to become an expert saver and build your wealth quickly.

6. The Risky Saver

The thrill of the deal is the Risky Saver at heart. This is the type of person who rolls the dice, throws caution to the wind and goes by the "you only live once" motto. It's not the allure of the money that is attractive to a Risky Saver so much as the rush that comes with trying something new — and possibly dangerous.

The Risky Saver is more interested in going on an adventure than putting money away for a rainy day. Traditional ways to save money — budgeting, clipping coupons, bargain hunting, etc. — aren't the usual habits of this money personality. Living by the high-risk, high-reward motto, the Risky Saver counts on his high-stakes investments to bring in the cash to save for big-ticket items.

This impulsive personality can cause problems in relationships, however. When one partner wants to budget, save and plan for future large expenses — like college tuition for their children or retirement — and the other wants to splurge on a shaky business idea or an investment, conflict usually results. The Risky Saver might seem carefree, but living in the moment can mean a lack of savings and poor financial standing in the future.

Instead of counting on investments or risky get-rich schemes, the Risky Saver should focus on growing their money safely. If you're a Risky Saver, consider a test drive with certificate of deposit accounts. Offering significant returns and little risk, these CD accounts can grow your savings.

5. The Short-Term Saver

Slightly better than the Risky Saver, the Short-Term Saver is, essentially, a spender who will save money for only a short period of time in order to get what they want quickly. If you fall into this group, you probably prefer fun over saving money.

This type of saver gets a thrill from the instant gratification of a purchase. They only save for short-lived experiences and to purchase material things, such as clothes, shoes and jewelry. They might have a long-term savings or retirement account, but chances are the balance is hovering near $0. Little foresight is given to the future, and they tend to talk themselves into believing they don't need to worry about their ultimate financial goals — such as retirement and purchasing a home.

However, they do understand the budgeting concept. And, they're fully aware of their monthly income and expenses. But sticking to any sort of financial plan for longer than a month is another story.

Still, they tend to feel regretful when the bills show up in the mail and the money has already been spent on clothes, the latest electronic gadgets and lunches out with friends. If you notice that you tend to only save money for a few weeks just so you can buy the latest handbag or iPhone, it's time to reevaluate your savings habits.

Don't Miss: 30 Essential Money Habits You Need to Master

4. The Single-Minded Saver

Having a financial goal is a step in the right direction. But the Single-Minded Saver might run into problems in the long run by only focusing on one area of financial preparedness.

For example, the Single-Minded Saver might be excellent at reducing frivolous spending in order to put funds away every week for an upcoming vacation. But at the same time, they aren't thinking about the ways to save money for financial basics, like establishing an emergency fund or saving for retirement.

Perhaps it's because the Single-Minded Saver isn't aware of the vulnerabilities they're creating. It's likely they're so focused on just one goal that they don't see any flaws in their plan. And the reality might not set in until an actual emergency happens, such as getting laid-off from a job or having to pay for a large medical expense. At that point, it will be too late, and they get hit with tons of debt that will take years to pay off.

There's nothing wrong with having one specific goal that you really want to meet, such as taking a scuba-diving trip in Australia or attending the Super Bowl in person with a bunch of friends. However, don't neglect or sacrifice your other financial responsibilities. It might take a little longer to reach your one, big goal, but when you return from that great trip across the Andes, you will come home to a secure financial infrastructure.

See: 9 Simple Steps to Save a $10,000 Emergency Fund

3. The Frugalist (or the Tightwad)

No matter if they're called frugal, cheap or a tightwad, this saving personality is the opposite of a spender. Simply put, spending money is not fun, and it might even bring about a feeling of anxiety for this saving personality. Unlike the savers mentioned earlier, the Frugalist usually keeps their money in the bank instead of burning through a paycheck frivolously.

This type of saving personality likes to have cash on hand for an emergency or to take a vacation. They sacrifice in one area — usually material items, such as clothing or golf clubs — in order to have the necessary funds for their mortgage or kids' college education. Friends might not understand the Frugalist's money habits, which can cause a feeling of isolation. However, knowing that they will be well prepared for retirement comforts the proverbial tightwad.

The Frugalist doesn't see themselves as being cheap, however. Instead, they think they're being smart with their money. After all, money is a source of survival, not enjoyment, to the Frugalist. Clipping coupons, shopping sales and hitting up yard sales are common practices for this savings personality type. They will cut corners wherever possible and will always choose a lower price over a higher-quality item. Unfortunately, though, cutting corners sometimes means paying more money in the long run.

2. The Clueless Saver

It's not that this group is actually "clueless," so to speak, but more that they are beginners when it comes to personal finance. For example, new college graduates who are embarking out into the world on their own for the first time are typically Clueless Savers.

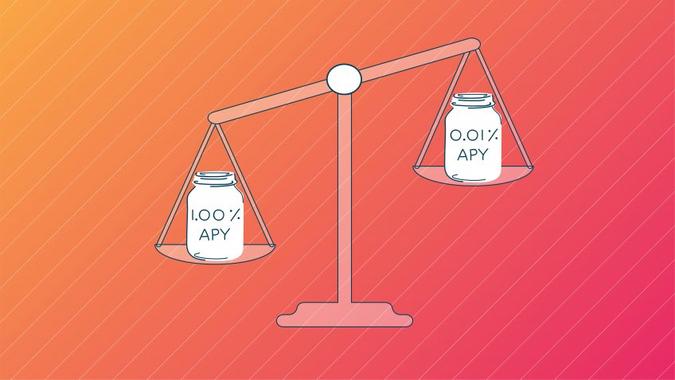

Often, the main challenge for the Clueless Saver is finding a way to balance their expenses with their savings goals. Those who fall into this category probably have a checking and savings account, and maybe even a credit card. But, they're unaware of the fees and interest rate they are paying.

For example, when it comes to choosing the best savings account, they might choose an account with a lower APY instead of an account with a higher APY. But it's because they simply don't know that the higher their savings account's APY, the faster their money can grow.

The Clueless Saver should dedicate time to learning the basics of personal finance. Actions like creating an emergency fund, establishing a monthly budget, paying off credit cards on time and thinking about retirement can help this group gain a solid financial foundation.

Test Yourself: Many Americans Don't Know These Basic Financial Terms — Do You?

1. The Money Master

They might be called "money hoarders" from time to time, but really, the Money Master has just done what the name says: mastered money. Through hard work, dedication and an eye on the future, this saver is able to meet their various long-term financial goals.

Top-ranked savers, Money Masters know how to master the many ways to save money. They're experts at budgeting and are not easily swayed by shoe sales or the latest gadgets. Their idea of instant gratification is clipping coupons, buying in bulk, regularly checking their 401k statements and continuously depositing cash into their high-interest savings accounts.

As for their financial goals, they keep their sights on buying a home, creating an emergency fund and building a comfortable retirement nest. But, they also save for short-term savings goals, like going on a family vacation.

These ultimate savers are also in the driver's seat when it comes to investing and are well educated on asset allocation, stocks and funds. While they have a diverse portfolio, they prefer safer investments that are steady earners. This group knows that a solid investing plan is one that is long-term.

Overall, the Money Master is a savings expert. Although it might take you a while to master their savings skills, it's never too late to start.

Up Next: How You Can Live Rich and Still Save Money

About the Author

How Much Money Does A Disabled Person Get

Source: https://www.gobankingrates.com/saving-money/savings-advice/which-money-personalities-are-you/

Posted by: mertzaffecke.blogspot.com

0 Response to "How Much Money Does A Disabled Person Get"

Post a Comment